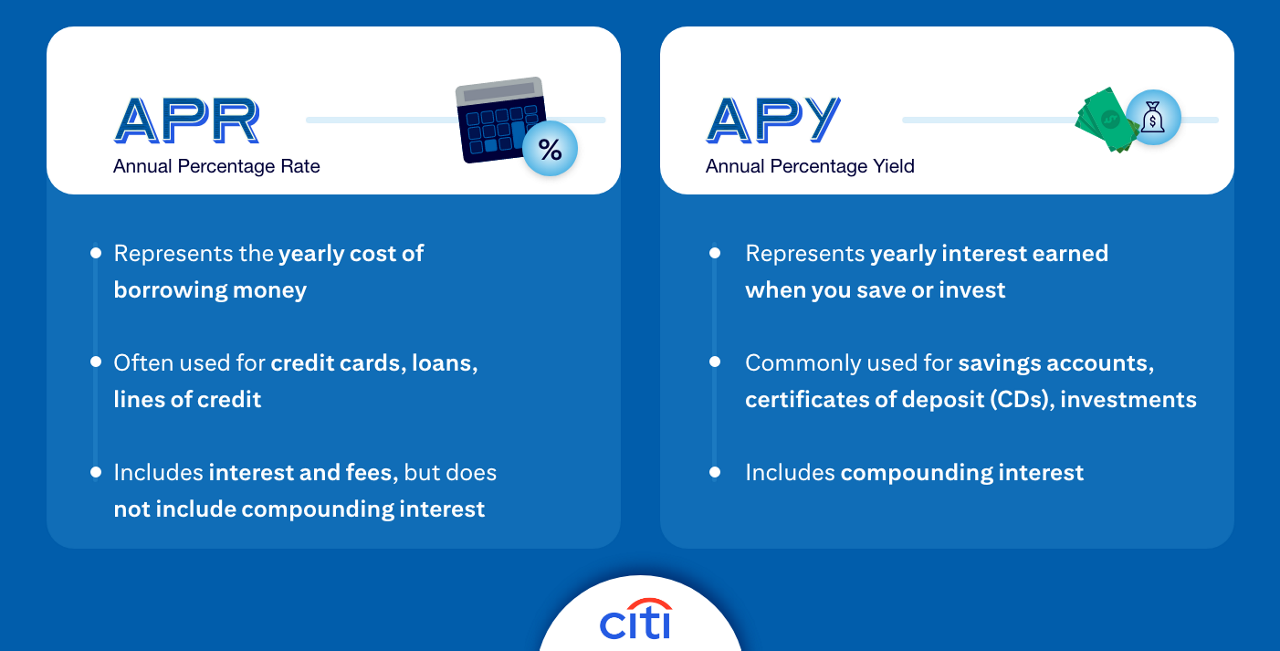

When you apply for a loan or a credit card, the cost of borrowing over time is expressed as the annual percentage rate or APR.

APR is a key factor to consider when choosing a lender. Understanding what goes into an APR can also help you choose a lender that meets your financial needs.

Here are 7 things to know about APR.

1. APR and interest rate are not always the same

APR can include both the interest rate and other costs of borrowing. For some loans and mortgages, for example, the APR will include certain costs associated with a loan, such as points or origination fees.

Credit card APRs, on the other hand, do not factor in annual or other fees. APRs are simply the interest rates applied to different balances on the card, such as purchases, cash advances and balance transfers.

2. Your annual percentage rate may increase with a late payment

Credit card issuers are required to comply with federal laws that offers protections to consumers. For example, credit card issuers are not allowed to increase your rate during the first year after the account is opened, but there are some exceptions. If you're over 60 days late on making a minimum payment, your issuer may have the right to raise your rate, even if you took advantage of a low intro APR.

3. You can try to (temporarily) avoid a high APR with a balance transfer

If you're carrying a credit card balance with a high APR, it may make sense to take advantage of a low intro APR offer on balance transfers with another credit card. Use the introductory rate period – often anywhere from 12 to 21 months – to try to pay off your debt. Remember, when deciding whether to use a balance transfer, weigh the costs, such as any balance transfer fees.

4. You can have different APRs for different types of balances on your credit card

You typically have a different APR for a purchase balance versus other types of balances, like cash advances. This affects the interest rates that are applied to different transactions made with your credit card.

For instance, if you have a low intro rate on purchases but you take out a cash advance, the amount you’ve withdrawn is subject to the cash advance APR instead of the low intro APR.